Mortgage Pre-Approval vs Pre-Qualification

Pre-approval and pre-qualification are often used interchangeably, but they are not the same. Understanding the difference affects how competitive your offer is, how sellers perceive your financing, and how predictable your path to closing will be. This guide explains how each works and when each one makes sense.

Get Pre-Approved or Talk to a Loan Expert

What Is Mortgage Pre-Qualification?

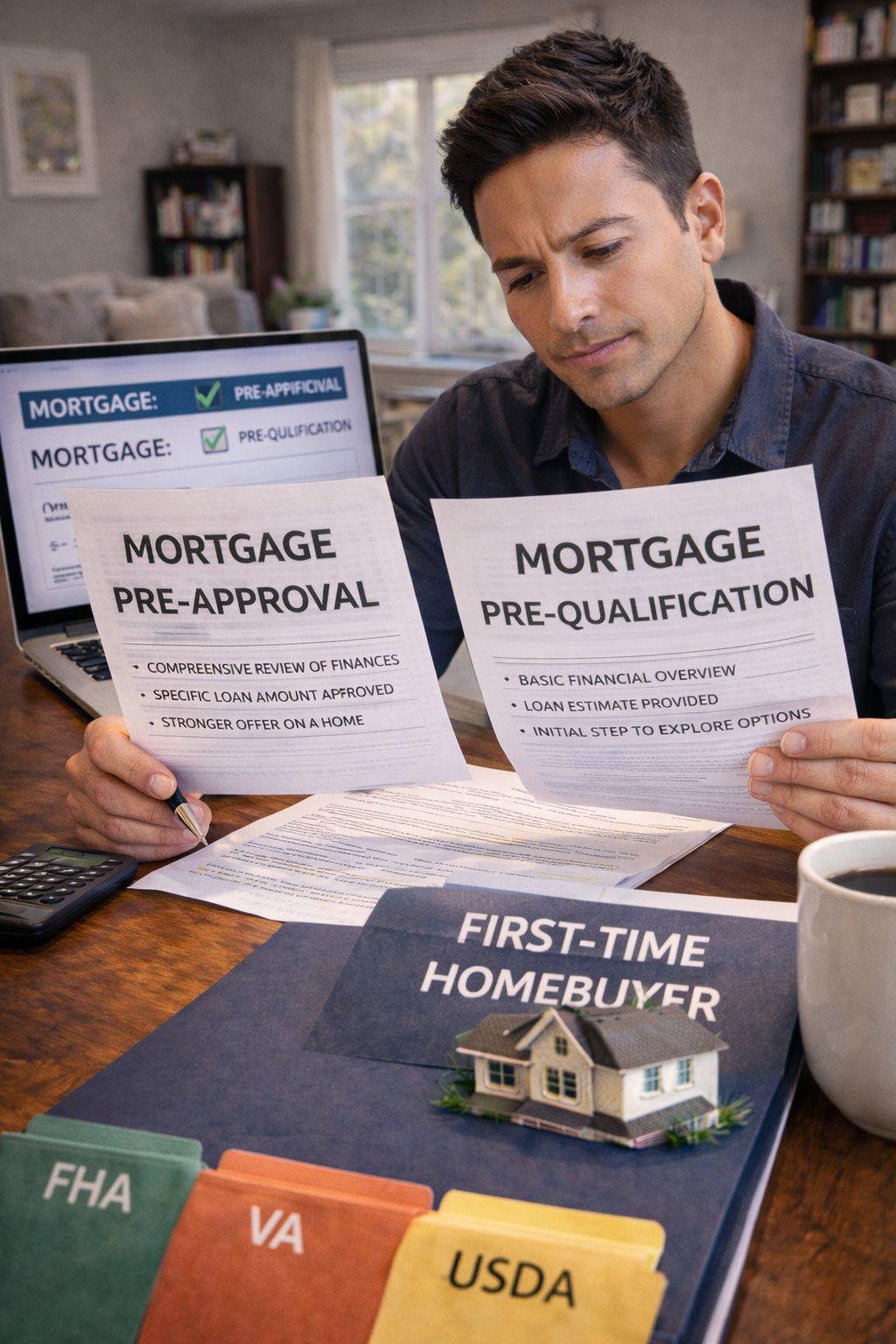

Pre-qualification is an informal estimate of what you may be able to borrow based on information you provide. It does not involve document verification or underwriting review.

- Based on estimated income, debts, and credit

- No document verification

- Typically no credit pull or a soft inquiry

- Useful for very early planning only

What Is Mortgage Pre-Approval?

Pre-approval is a formal review of your financial profile. Income, assets, credit, and debts are verified and evaluated against loan guidelines. This is the level sellers expect when you are making offers.

- Income and assets documented

- Credit report reviewed

- Underwriting guidelines applied

- Pre-approval letter issued for offers

Pre-approval is also the starting point for the full mortgage process. If you want to understand what happens after pre-approval, see how long it typically takes to close a mortgage.

Pre-Approval vs Pre-Qualification Comparison

| Feature | Pre-Qualification | Pre-Approval |

|---|---|---|

| Purpose | Early estimate | Offer-ready review |

| Documentation | None or minimal | Income, assets, credit verified |

| Credit Check | None or soft pull | Full credit review |

| Seller Confidence | Low | High |

| Offer Strength | Weak | Strong |

When Pre-Qualification Makes Sense

- You are just starting to explore home prices

- You want a rough affordability estimate

- You are not preparing to make offers yet

When Pre-Approval Is the Better Choice

- You are actively house hunting

- You plan to make offers soon

- You want accurate buying power numbers

- You want fewer financing surprises later

Buyers often underestimate what happens between pre-approval and closing. Understanding the full process helps you avoid delays. Our mortgage closing timeline guide walks through each step.

Common Pre-Approval and Pre-Qualification Myths

- “Pre-qualification guarantees approval” — it does not

- “Pre-approval locks my interest rate” — rate locks are separate

- “Pre-approval hurts credit significantly” — impact is usually minimal

Related Buyer Mortgage Guides

- Mortgage Pre-Approval Guide

- How Long Does It Take to Close a Mortgage?

- How Much House Can I Afford?

- Buyer Mortgage Guides Hub

Get Pre-Approved With Confidence

Moving from estimation to pre-approval gives you clearer numbers, stronger offers, and a smoother path to closing.

This page is for educational purposes only and is not a commitment to lend. Loan terms, documentation requirements, and timelines vary by borrower and lender.

Recent Comments