FHA vs Conventional Loans: Which Mortgage Is Right for You?

FHA and conventional loans are two of the most common mortgage options for homebuyers. The right choice depends on your credit profile, down payment, property type, and long term goals. This hub page explains the key differences at a high level and links to state specific comparisons where you can see local context and next steps.

Quick Summary

- FHA loans often appeal to buyers who want down payment flexibility or a more forgiving credit approach.

- Conventional loans are frequently a better fit for borrowers with stronger credit or larger down payments.

- The best option is the one with the strongest approval profile and the lowest long term cost for your situation.

What Is an FHA Loan?

An FHA loan is insured by the Federal Housing Administration. FHA financing is designed to make homeownership more accessible through standardized underwriting guidelines and flexible qualification criteria for many buyers.

What Is a Conventional Loan?

A conventional loan is not insured by a government agency and is typically underwritten under guidelines established by Fannie Mae and Freddie Mac. Conventional financing often rewards stronger credit profiles and can provide more flexibility in mortgage insurance structure. For a deeper overview, see our Conventional Loans guide.

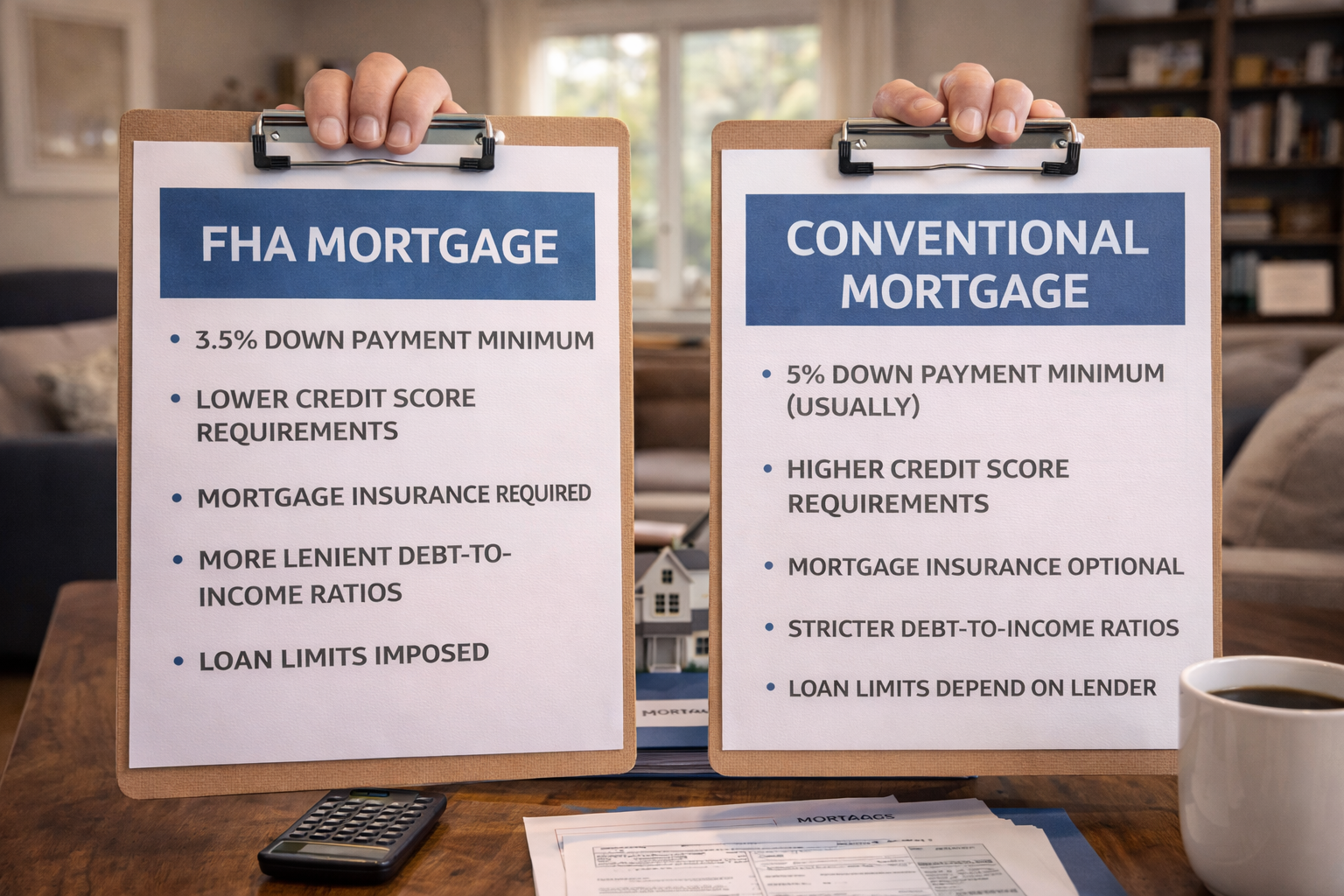

Key Differences (High Level)

| Feature | FHA | Conventional |

|---|---|---|

| Down payment flexibility | Often more flexible for qualified borrowers | Often rewards larger down payments |

| Credit guidelines | Generally more forgiving of past credit issues | Typically stricter credit expectations |

| Mortgage insurance | Required under FHA guidelines | May be removable under certain conditions |

| Property standards | Includes FHA appraisal standards | Standard conventional appraisal |

| Best fit (common scenarios) | Buyers prioritizing qualification flexibility | Buyers optimizing long term cost and flexibility |

Your down payment strategy is often the swing factor between FHA and conventional options. Review practical scenarios, gift funds, and low down payment paths in our Down Payment Options guide.

Mortgage insurance is another major difference. See our Mortgage Insurance Explained guide for the full breakdown.

How to Choose Between FHA and Conventional

The best way to decide is to compare both options side by side using your actual borrower profile. Approval strength, monthly payment structure, and total cost over time can vary significantly based on credit, down payment, and property characteristics.

Many buyers work with a mortgage broker at this stage to model both scenarios and avoid choosing a loan based on approval alone.

Primary Residence vs Investment Property

FHA loans are designed for owner occupied primary residences. Conventional loans can be used for primary homes, second homes, and in many cases investment properties, but the guidelines and down payment expectations change for rentals.

If you are buying a rental or converting a future home into a rental, use our investor hub: Investor Financing. For conventional investment comparisons, see DSCR vs conventional investment loans and DSCR loan requirements.

Using Rental Income and Property Cash Flow

Conventional underwriting for primary residences is based on your personal income and debts. Investment financing often places more weight on rental income, reserves, and property cash flow. If you plan to use rents to support qualification, review using rental income to qualify.

If your property is titled in an entity, start here: LLC mortgage loans. If your long term plan is to scale past a few properties, see portfolio loans explained.

FHA, Conventional, and Future Refinance Options

The loan you choose today does not lock you into the same structure forever. Many homeowners who start with FHA later refinance into a conventional loan as equity builds, credit improves, or market conditions change.

Homeowners often explore how mortgage refinancing works, evaluate when refinancing makes sense, or compare rate and term options to reduce long term interest costs and adjust monthly payments.

If you are refinancing an investment property, the strategy can be different. For investor specific equity planning, see investor cash out refinance.

FHA vs Conventional by State

Select your state below for a detailed comparison with local context, common questions, and next steps.

Compare FHA vs Conventional for Your Situation

We also review conventional pricing, down payment scenarios, refinance pathways, and mortgage insurance tradeoffs so you can choose the lowest cost path with the strongest approval profile. If you are buying a rental or planning a BRRRR style strategy, we can also map investor options like DSCR, portfolio, and LLC financing.

Get Started Contact 360 MortgageRelated Mortgage Guides

- FHA Loans Overview

- Conventional Loans

- Mortgage Refinance Overview

- When to Refinance a Mortgage

- Mortgage Pre Approval Guide

- First Time Homebuyer Programs

- Buyer Decision Tools

- Investor Financing Hub

- BRRRR financing guide

Disclaimer: This page is for informational purposes only and does not constitute a commitment to lend. Loan programs, eligibility, and underwriting requirements are subject to change. Contact 360 Mortgage for current guidelines and a personalized qualification review. NMLS 80777.

Recent Comments