What DSCR Means (In Plain English)

DSCR stands for Debt Service Coverage Ratio. It’s a way to measure whether a property’s income can comfortably cover the monthly housing expense. In DSCR lending, the property is the star of the show: the lender focuses on the rental cash flow more than your personal income.

If you want the program overview (who it’s for, typical requirements, eligible property types), see the main page: DSCR Loans.

DSCR Formula

The most common DSCR calculation looks like this:

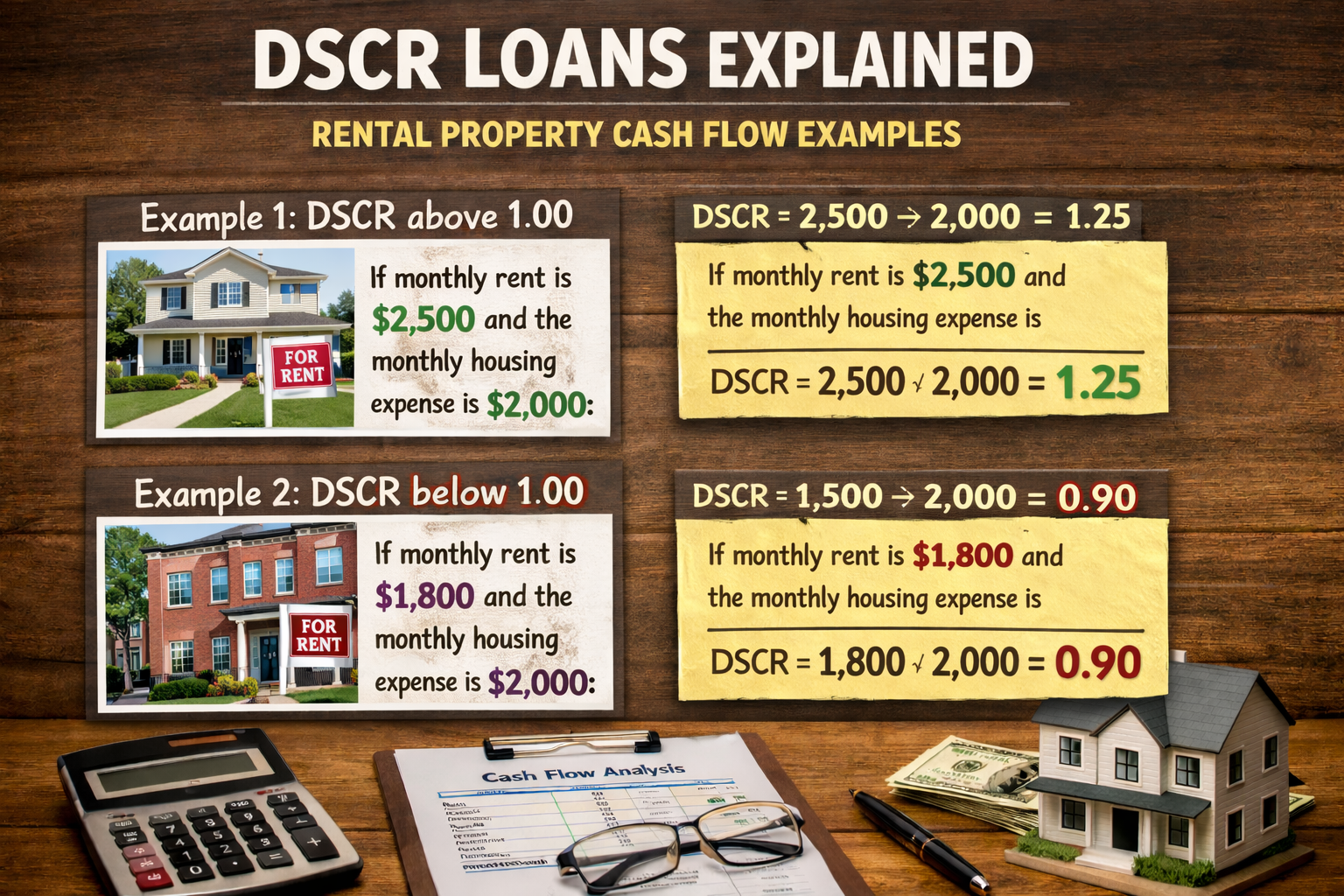

- DSCR = Monthly Rental Income ÷ Monthly Housing Expense

A DSCR of 1.00 means the income covers the expense exactly. A DSCR above 1.00 indicates positive coverage. Some programs allow lower ratios with compensating factors (such as higher down payment, higher credit score, or stronger reserves).

What Counts as Income for DSCR

Lenders typically base income on either documented rent or a market-rent estimate.

- Existing lease rent: If the property is currently rented and the lease is acceptable

- Market rent estimate: Often supported by an appraisal rent schedule (when required)

- Short-term rental income: Program-dependent; may require additional documentation and market support

If you are evaluating short-term rentals, also see: Short-Term Rental Financing.

What Counts as Debt Service (Monthly Housing Expense)

In most programs, “debt service” means the full monthly housing payment tied to the property:

- Principal and interest

- Property taxes

- Homeowners insurance

- HOA dues (if applicable)

- Mortgage insurance (if applicable)

DSCR Examples

Common Underwriting Scenarios (What Investors Run Into)

- Vacant property purchase: Qualification may rely on market rent estimates

- Rents rising faster than taxes/insurance: DSCR can improve after stabilization

- Higher insurance/HOA: Can materially reduce DSCR even if rent is strong

- Short-term rentals: Documentation varies widely; underwriting is more conservative

If you’re building a long-term buy-and-hold portfolio, see: Rental Property Financing and BRRRR Financing Guide.

DSCR Loans vs Conventional Investor Loans

Conventional investor loans typically underwrite your personal income and debt-to-income ratio. DSCR loans lean more heavily on property cash flow and reserves.

- Conventional: Personal income documentation + DTI-driven underwriting

- DSCR: Cash-flow-driven underwriting focused on rental income vs housing expense

For the main DSCR overview and qualification checklist, go back to DSCR Loans.

DSCR Loans Explained: FAQs

Is DSCR calculated using gross rent or net cash flow?

Most programs use a rent-based calculation compared against the full monthly housing expense. Program details vary by lender.

Can I get a DSCR loan if I already own multiple properties?

Often yes. DSCR loans are commonly used for scaling portfolios, depending on reserves and program limits.

Do DSCR loans work for BRRRR?

Many investors use DSCR financing as part of the BRRRR strategy, depending on property seasoning rules and the lender’s refinance guidelines. See: BRRRR Financing Guide.

Next Steps

If you’re ready to price out a deal or sanity-check DSCR eligibility, the fastest path is to share the address, estimated rent, and purchase terms. We’ll confirm your options and likely DSCR fit.

Related Investor Financing Pages

Disclosure: This page provides general information and is not a commitment to lend. DSCR loan programs, rates, guidelines, and requirements vary by lender and are subject to change. Qualification depends on underwriting and complete documentation review.

NMLS: 80777

Licensed mortgage broker in Missouri, Kansas, and Louisiana.

Recent Comments