DSCR Loans for Single Family Investment Properties

Single family homes remain one of the most popular types of rental property in the country. Many investors use DSCR loans to finance these properties because qualification is based primarily on the property’s rental income rather than the borrower’s personal tax returns.

For investors who want to buy, refinance, or scale a portfolio of single family rentals, DSCR financing can offer a flexible path that aligns more closely with how investment properties actually perform.

If you are new to this loan type, start with our guides on what DSCR means and how DSCR loans work.

Single family rentals are often the easiest entry point for investors because they are familiar, widely available, and easier to value than more complex property types. That simplicity makes them a common fit for DSCR financing.

Why Investors Use DSCR Loans for Single Family Rentals

Traditional investment property loans often require full income documentation, tax returns, and detailed debt to income analysis. That can create friction for investors who own multiple properties, write off expenses aggressively, or operate through LLCs.

DSCR loans are popular because they are designed around the performance of the rental property itself. Instead of focusing mainly on the borrower’s employment income, the lender looks at whether the property generates enough rent to support the monthly debt payment.

That makes DSCR financing especially attractive for investors who want to:

- Purchase a long term rental home

- Refinance an existing single family rental

- Pull cash out to buy additional properties

- Scale a portfolio more efficiently

- Use entity ownership such as an LLC when allowed

Related pages in this cluster:

- DSCR loans for rental property

- DSCR cash out refinance

- Scaling a rental portfolio with DSCR loans

- DSCR loans for LLC borrowers

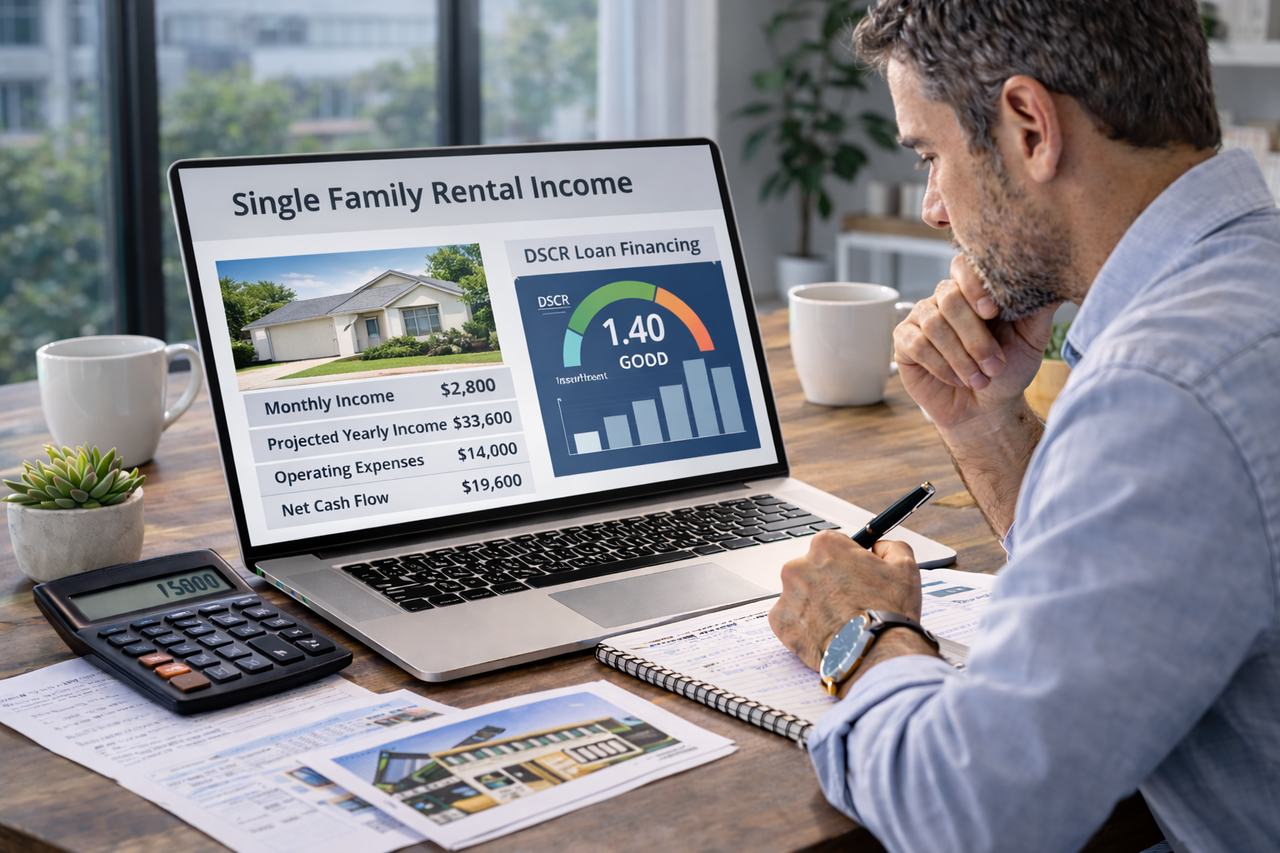

How DSCR Works on a Single Family Investment Property

The lender calculates the Debt Service Coverage Ratio by comparing the property’s rental income to its total monthly debt obligation. In simple terms, the lender wants to know whether the rent from the property can support the payment.

A stronger ratio generally means the property is producing more income relative to the payment. A weaker ratio may still qualify in some programs, but often with tighter terms or larger down payment requirements.

For more detail, explore:

Single family rentals often work best when investors choose neighborhoods with durable tenant demand, stable employment drivers, and rent levels that support both cash flow and long term appreciation. A good property is not just one that qualifies. It is one that still performs after vacancy, maintenance, and future market changes are considered.

How Rent Is Evaluated for Single Family Rentals

Lenders usually evaluate income using current lease agreements, market rent analysis, or appraiser supported rent estimates. On many transactions, the appraisal includes a market rent schedule that helps support the projected rental income used for qualification.

This is why investors should understand:

- Whether current rent is at market level

- Whether the property is occupied or vacant

- Whether rent is stable and documentable

- Whether nearby comparable rentals support the projected income

Related resources:

- How rent is used for qualification

- Form 1007 rent schedule

- Gross rent vs net rent

- How to analyze a rental property deal

A single family property can qualify on rent alone and still be a weak investment if taxes, insurance, repairs, vacancy, and turnover are underestimated. DSCR qualification is one screen. It is not the same thing as full investment analysis.

Benefits of Single Family Rentals for Investors

Single family homes are popular with both new and experienced investors because they offer a practical blend of stability, liquidity, and tenant demand.

Common advantages include:

- Large buyer and renter pool

- Simpler property management compared to larger assets

- Strong resale demand

- Easier financing and valuation in many markets

- Clear path for repeat acquisitions

For newer investors, these properties can be an easier starting point than more complex investment types such as multifamily or short term rentals.

You may also want to compare:

- DSCR loans for first time investors

- DSCR loans for multifamily properties

- DSCR loans for condo investments

- DSCR loans for short term rentals

Typical DSCR Loan Requirements for Single Family Rentals

Requirements vary by lender, but most DSCR programs for single family rentals revolve around the same major underwriting categories.

- Credit score

- Down payment or equity position

- Maximum loan to value

- Reserve requirements

- Minimum acceptable DSCR ratio

For deeper guidance, review:

- DSCR loan requirements

- Credit score requirements

- Down payment requirements

- LTV limits

- Reserve requirements

- No income verification investor loans

- DSCR loans with no tax returns

- Single family rentals are one of the most common uses for DSCR loans

- Qualification is based heavily on the property’s rent and debt service ratio

- These properties are often easier to buy, finance, and resell than more complex asset types

- Cash flow analysis still matters beyond basic loan approval

Cash Flow Risks to Watch on Single Family Rentals

Single family rentals are often simpler than larger properties, but they still carry real risks. Because one tenant supports the whole property, a vacancy immediately drops rental income to zero.

Investors should model:

- Vacancy periods

- Repairs and maintenance

- Insurance increases

- Tax increases

- Turnover and leasing costs

These resources can help investors underwrite more carefully:

- Rental property cash flow

- Rental property expenses list

- Rental property break even analysis

- Risk analysis for rental properties

- What is a good cash flow on a rental property

Many investors build wealth by repeating a straightforward model: buy one strong single family rental, stabilize it, improve rents where justified, then use accumulated equity and cash flow to acquire the next property. DSCR loans are often well suited to this step by step portfolio building approach.

Using DSCR Loans to Build a Portfolio of Single Family Homes

Single family rentals are often the foundation of a larger portfolio. They are familiar to most investors, flexible across many markets, and easy to understand operationally.

As your holdings grow, these pages become especially relevant:

- Scaling a rental portfolio

- How many properties can you buy

- DSCR cash out refinance

- Building a rental property portfolio

- How many rentals do you need to retire

- When a rental property becomes passive income

As rental portfolios grow, strong operational systems become essential. Investors looking for guidance on tenant screening, leasing strategies, property management, and landlord best practices can explore the educational resources available at Blue Castle Management.

DSCR Loans vs Conventional Financing for Single Family Investments

Conventional investor loans can work well for some borrowers, especially early in their investing journey. But as portfolios grow, conventional rules around personal income, tax returns, financed property limits, and debt to income ratios can become restrictive.

That is why many investors compare DSCR financing against other options such as:

- DSCR loans vs conventional investor loans

- DSCR loans vs portfolio loans

- DSCR loans for self employed investors

- DSCR loans for lower credit score investors

Talk With a DSCR Loan Specialist About Single Family Rental Financing

If you are buying or refinancing a single family rental property, a DSCR loan may allow you to qualify based on the property’s rental income rather than personal tax returns.

We help real estate investors structure financing for single family rentals, portfolio expansion, and cash out refinance strategies.

Talk With an Investor Loan Specialist

DSCR and Investor Loan Guidance

Talk Through DSCR Loan Options With Lyndi Gajan

Real estate investors can work with Lyndi Gajan to talk through DSCR loan questions, rental income scenarios, refinance options, and investor documentation before choosing a loan path.

Lyndi Gajan NMLS ID 88249. 360 Mortgage Inc. NMLS ID 80777. Loan availability, licensing, and guidelines vary by state, property, and loan purpose.

Frequently asked questions

Who is DSCR Loans for Single Family Investment Properties best for?

DSCR Loans for Single Family Investment Properties may fit borrowers whose goals, documentation and property details line up with the program requirements. A mortgage review is the fastest way to compare options without relying on generic assumptions.

What documents should I prepare?

Most borrowers should be ready to discuss income, assets, debts, credit history, property details and the purpose of the loan. Exact documentation depends on the program and underwriting review.

What is the next step?

The next step is to talk with 360 Mortgage so the team can review your situation, explain available options and outline the application path.