How Much Equity Do You Need to Refinance a Home?

Home equity plays a central role in most refinance decisions. The amount of equity you have in your home helps determine whether you qualify for refinancing, what loan options are available, and how much money you may be able to access if you choose a cash out refinance.

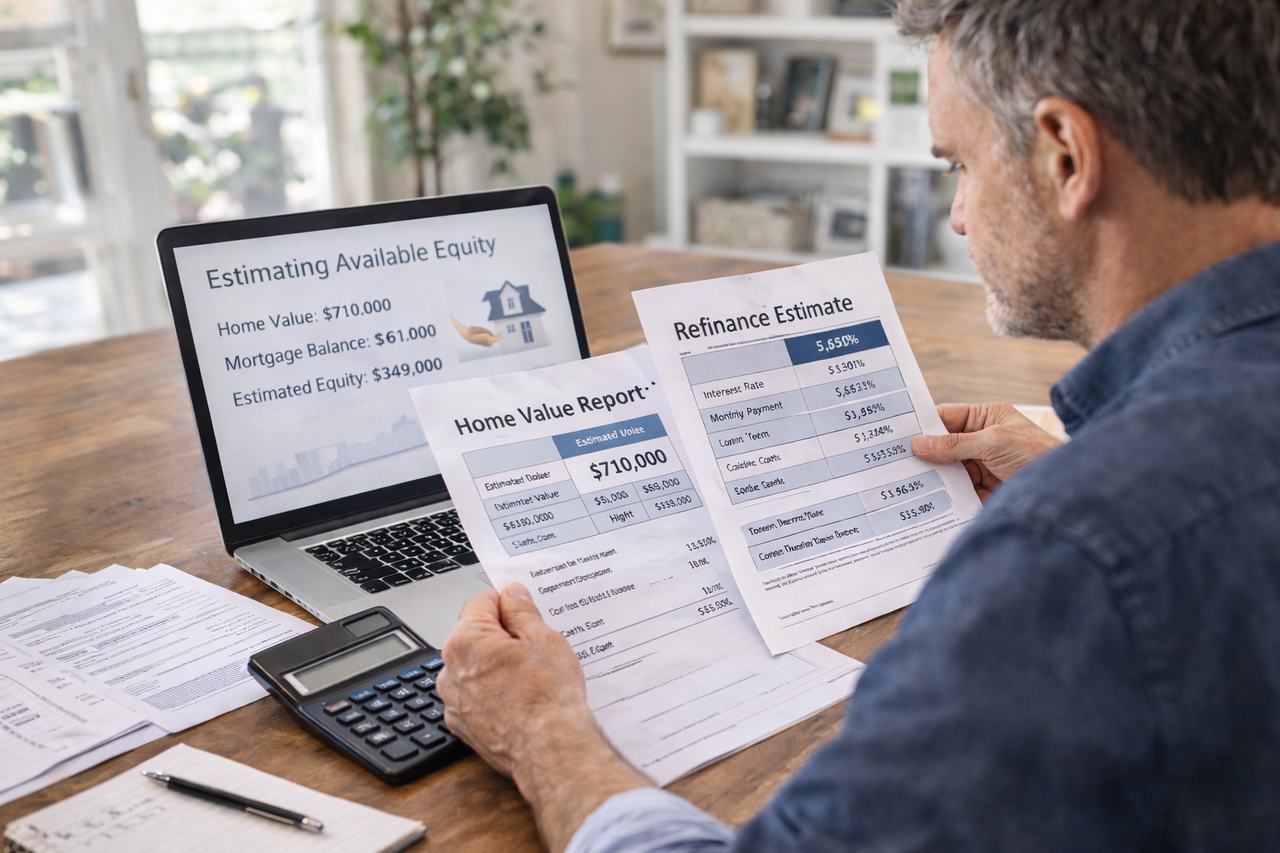

In simple terms, equity is the difference between your home’s current market value and the remaining balance on your mortgage.

This guide explains how lenders evaluate equity, how much equity is typically required to refinance, and how homeowners can estimate their own refinance eligibility.

For the full refinance hub, visit our Mortgage Refinance Guide.

What Is Home Equity?

Home equity represents the portion of your property that you truly own.

It is calculated by subtracting your remaining mortgage balance from your home’s current market value.

Example:

- Home value: $450,000

- Mortgage balance: $300,000

- Home equity: $150,000

In this example, the homeowner has built $150,000 in equity.

As mortgage balances decrease and property values increase over time, equity typically grows.

Loan to Value Ratio (LTV)

Lenders evaluate refinance eligibility using a metric called the loan to value ratio, often abbreviated as LTV.

The LTV compares the mortgage balance to the property’s current value.

Formula:

LTV = Loan Balance ÷ Property Value

Example:

- Mortgage balance: $300,000

- Home value: $400,000

- LTV: 75 percent

Lower LTV ratios typically make refinancing easier and may result in better loan pricing.

Typical Equity Requirements for Refinancing

The amount of equity required depends on the type of refinance being considered.

Rate and Term Refinance

When refinancing simply to change the interest rate or loan term, lenders often allow loan to value ratios up to about 95 percent in certain programs.

This means homeowners may be able to refinance with as little as about 5 percent equity depending on the loan program.

Related page: Conventional Rate and Term Refinance

Cash Out Refinance

Cash out refinancing typically requires more equity because the borrower is withdrawing funds from the property.

Many conventional loan programs limit cash out refinancing to about 80 percent of the home value.

Example:

- Home value: $500,000

- Maximum refinance loan at 80 percent: $400,000

- Current mortgage balance: $300,000

- Potential cash available: about $100,000 before costs

Related page: Cash Out Refinance Overview

Equity Requirements for Investment Property Refinancing

Investment property refinancing typically requires stronger equity positions.

Many lenders limit loan to value ratios for investment property cash out refinancing to approximately 70 to 75 percent.

This means investors generally need at least 25 to 30 percent equity to complete a cash out refinance.

Related page: Cash Out Refinance for Investment Property

How to Estimate Your Home Equity

Homeowners can estimate equity by reviewing recent sales of comparable homes in their area or by using online home value tools.

A refinance lender will typically confirm the property value through a professional appraisal during the loan process.

To estimate your equity:

- Estimate your home’s current value.

- Check your current mortgage balance.

- Subtract the mortgage balance from the estimated home value.

This provides an approximate equity estimate before the lender orders an appraisal.

Why Equity Matters in Refinancing

Equity affects several important aspects of refinancing.

Loan Approval

Higher equity levels make approval easier because the lender faces less risk.

Interest Rates

Borrowers with lower loan to value ratios often receive better interest rates.

Mortgage Insurance

If the loan to value ratio falls below certain thresholds, homeowners may be able to eliminate private mortgage insurance.

Related page: Refinance to Remove PMI

Situations Where Homeowners Build Equity Faster

Several factors can increase equity over time.

- Making regular mortgage payments

- Property values increasing in the local market

- Making additional principal payments

- Completing renovations that improve home value

These factors may improve refinancing opportunities.

What Happens If You Have Very Little Equity?

Some homeowners consider refinancing even when equity levels are limited.

In certain situations, specialized programs may still allow refinancing if other qualification factors are strong.

However, limited equity may reduce available options or result in stricter lending requirements.

Related pages:

Other Factors That Affect Refinance Eligibility

While equity is important, lenders also evaluate other factors when approving a refinance.

- Credit score

- Income stability

- Debt to income ratio

- Property condition

- Payment history on the existing mortgage

Strong financial profiles can sometimes offset slightly lower equity levels.

Related page: Cash Out Refinance Requirements

Location Based Refinance Resources

If you are considering refinancing, local property values and lending conditions may affect your options.

Explore refinance resources in your area:

- Florida Mortgage Refinance

- Missouri Mortgage Refinance

- Kansas Mortgage Refinance

- Louisiana Mortgage Refinance

- Tennessee Mortgage Refinance

Talk With 360 Mortgage About Your Refinance Options

Understanding how much equity you have is one of the first steps in evaluating refinance options. A mortgage broker can review your loan balance, estimated property value, and financial profile to determine which refinance programs may be available.

Contact 360 Mortgage to discuss your refinance options.

Return to the refinance hub here: Mortgage Refinance Guide

Frequently asked questions

Who is How Much Equity Do You Need to Refinance a Home? best for?

How Much Equity Do You Need to Refinance a Home? may fit borrowers whose goals, documentation and property details line up with the program requirements. A mortgage review is the fastest way to compare options without relying on generic assumptions.

What documents should I prepare?

Most borrowers should be ready to discuss income, assets, debts, credit history, property details and the purpose of the loan. Exact documentation depends on the program and underwriting review.

What is the next step?

The next step is to talk with 360 Mortgage so the team can review your situation, explain available options and outline the application path.