FHA vs Conventional Loans in Florida

Choosing between an FHA loan and a conventional mortgage is one of the most common decisions Florida homebuyers face. Both options can work well depending on your credit profile, down payment, and long term goals but they are designed for different types of borrowers.

This guide compares FHA and conventional loans in a Florida context so you can understand how each option works, when one may make more sense than the other, and how to decide before you get pre approved.

Quick Answer

FHA loans often appeal to buyers who want lower down payment flexibility or more forgiving credit guidelines. Conventional loans are frequently a better fit for borrowers with stronger credit profiles or larger down payments. The best choice depends on total cost, not just approval.

FHA and conventional loans can produce very different monthly costs once mortgage insurance, taxes, and insurance are included. Comparing those payments against rent can help clarify timing.

Run the Florida Rent vs Buy CalculatorWhat Is an FHA Loan?

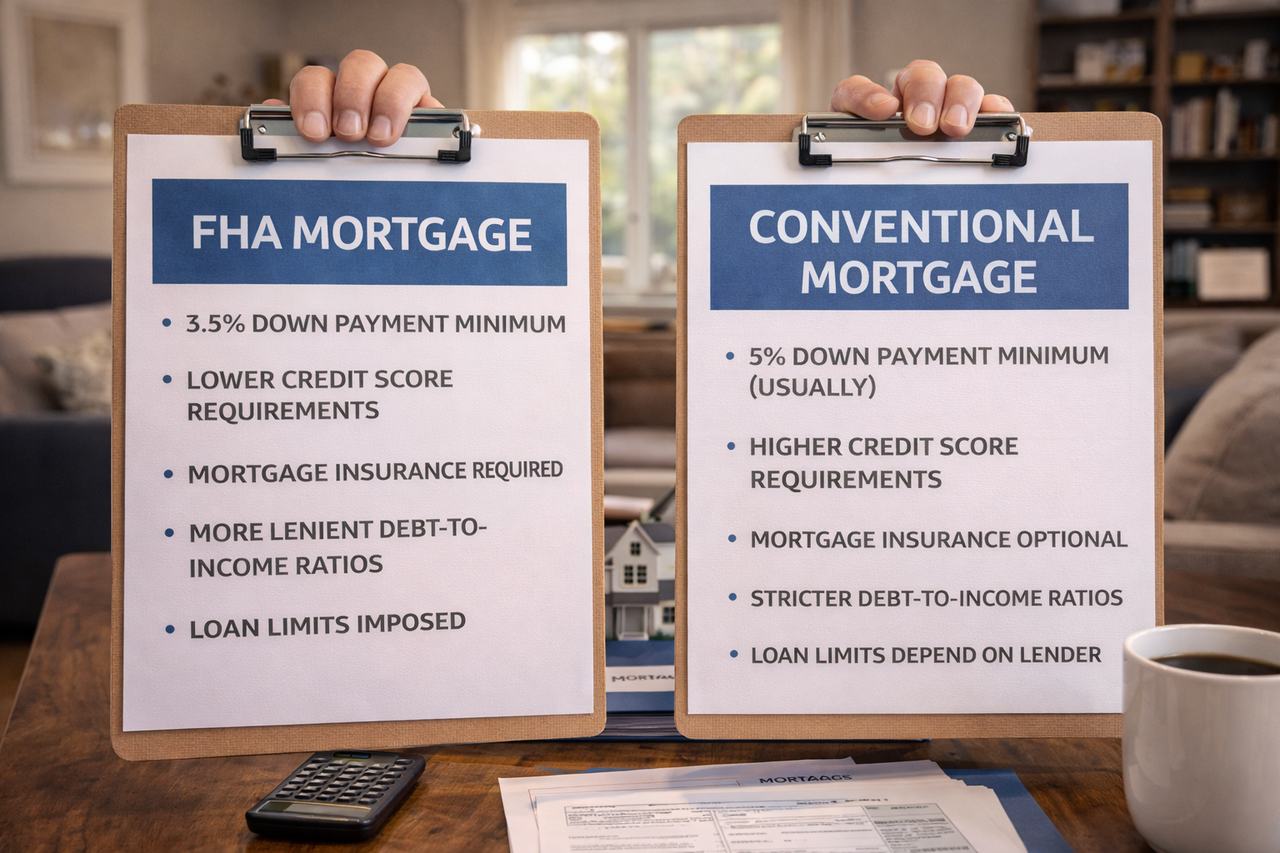

An FHA loan is a mortgage insured by the Federal Housing Administration. FHA loans are designed to make homeownership more accessible by allowing qualified buyers to purchase with more flexible credit standards and standardized underwriting guidelines.

FHA loans are commonly used by first time homebuyers, but they are available to any qualified borrower purchasing an eligible primary residence in Florida.

What Is a Conventional Loan?

A conventional loan is not insured by a government agency and is typically underwritten according to guidelines set by Fannie Mae and Freddie Mac. These loans often favor borrowers with stronger credit profiles and more financial flexibility.

Conventional loans can offer advantages in long term cost structure, especially for buyers who qualify for favorable terms and want flexibility around mortgage insurance. For a full overview, see our Conventional Loans guide.

FHA vs Conventional Loans: Florida Comparison

| Feature | FHA Loan | Conventional Loan |

|---|---|---|

| Down payment flexibility | Often more flexible for qualified buyers | Typically rewards larger down payments |

| Credit guidelines | More forgiving of past credit issues | Generally stricter credit expectations |

| Mortgage insurance | Required under FHA guidelines | May be removable under certain conditions |

| Property standards | Includes FHA appraisal requirements | Standard conventional appraisal |

| Best suited for | Buyers prioritizing approval flexibility | Buyers optimizing long term cost |

Choosing Between FHA and Conventional in Florida

Florida’s housing market includes a wide range of property types, from coastal homes and condos to inland subdivisions and master planned communities. Both FHA and conventional loans are widely used across the state, but property type and insurance considerations can influence which option makes more sense.

- Condos: Some condominiums require additional eligibility review

- Insurance: Homeowners insurance and flood considerations may affect qualification

- Competition: Pre approval strength matters in competitive Florida markets

- Long term costs: Mortgage insurance structure can influence total cost over time

Since mortgage insurance is often the biggest cost difference between FHA and conventional, review the details in our Mortgage Insurance Explained guide.

How to Decide Which Loan Is Right for You

The best way to choose between FHA and conventional financing is to compare both options side by side using your actual financial profile. Approval alone doesn’t tell the full story. Total cost, flexibility, and long term goals matter just as much. If you are also deciding whether to buy now or keep renting, the Florida rent vs buy calculator lets you compare FHA and conventional style payments against your current rent over your expected time horizon.

Down payment strategy is another major swing factor. If you’re deciding how much to put down or using gift funds, start with our Down Payment Options guide.

A proper pre approval allows you to evaluate both loan types before making an offer, so you can move forward with confidence rather than assumptions.

Refinance Planning in Florida After You Buy

Many Florida buyers start with FHA because it can be easier to qualify with a smaller down payment, then refinance later if their credit improves, equity grows, or market conditions make a new loan structure more cost effective. This is common when homeowners want to remove monthly mortgage insurance, change their loan term, or adjust their payment strategy over time.

If you want to understand refinance at a high level, start with our Mortgage Refinance Guide. If you are trying to decide whether refinancing is worth it right now, review When to Refinance a Mortgage.

Compare FHA vs Conventional for Your Florida Purchase

We’ll review your goals, credit profile, and budget to help you compare FHA and conventional options clearly before you commit to a loan.

Get Pre Approved Contact 360 MortgageRelated Florida Mortgage Guides

- FHA Loans in Florida

- Conventional Loans

- Mortgage Refinance Guide

- When to Refinance a Mortgage

- Down Payment Options

- Mortgage Insurance Explained

- First Time Homebuyer Programs

- Mortgage Pre Approval Guide

Disclaimer: This page is for informational purposes only and does not constitute a commitment to lend. Loan programs, eligibility, and underwriting requirements are subject to change. Contact 360 Mortgage for current guidelines and a personalized qualification review. NMLS 80777.

Frequently asked questions

Who is FHA vs Conventional Loans in Florida best for?

FHA vs Conventional Loans in Florida may fit borrowers whose goals, documentation and property details line up with the program requirements. A mortgage review is the fastest way to compare options without relying on generic assumptions.

What documents should I prepare?

Most borrowers should be ready to discuss income, assets, debts, credit history, property details and the purpose of the loan. Exact documentation depends on the program and underwriting review.

What is the next step?

The next step is to talk with 360 Mortgage so the team can review your situation, explain available options and outline the application path.